Should you buy Alien Abduction Insurance?

because Behavioral Finance has some problems with the future...

Over 100,000 Americans have Alien Abduction Insurance. GEICO sold some. Lloyds of London underwrote 20,000. Two claims were paid.1

Behavioral Economists would hardly be surprised. After all, people are crazy.

Behavioral Economics, aka Behavioral Finance,2 was the app update to economics. Traditional economics had blind spots, treating human beings as perfectly rational when we clearly are not. Some people insure against UFOs.

These thinkers found the blind spots. Their exciting new theory explained why we did weird things with money: loss aversion (risking big losses to avoid small ones), mental accounting (hoarding credit card points for vacation instead of treating all money the same), or prospect theory (the Aliens).

Daniel Kahneman and Amos Tversky published the first paper in 1971 and their seminal work in 1979. Richard Thaler burst on the scene in the 1980s. Nobel Prizes and best selling books followed, so that by 2011 every smart person had to say they read Thinking Fast and Slow whether or not they finished it or even bought it. From there, we were all nudged and prompted into “choice architectures” that automatically enrolled us in retirement plans. Everything got “framed” as goals, not balance sheets. Generations were saved from their irrational selves.

Behavioral-Econ is now 55 years old. No less than 35 universities offer graduate degrees in the field. Just this week, the Behavioral Economics Guide 2026 began the move toward “Behavioral Economics 3.0,” a quest to integrate history (lived experience), biology, and AI into explaining why we do what we do. Before they go much farther, the historian in me feels compelled to offer a warning.

Behavior Economics has developed two blind spots of its own.

Mad Max and the Federal Reserve

Behavioral Econ showed that people treat rare events as more likely than they truly are (terrorist attacks, hyperinflation, actors and TV stars winning the presidency). Those things rarely happen.

Fools think with fear. Scholars think with Excel. We know the probabilities.

The opening essay of Behavioral Economics Guide 2026 skewers Henry Wallich, a 1970s-era Fed Governor, whose childhood experiences with German hyperinflation left him relentlessly hawkish. Wallich treated his lived experience with inflation as more important than the data presented to him. Nancy Teeters, his colleague, offers the supposed voice of modern reason: “Henry Wallich was our real problem.”3

But Wallich was right and Teeters was wrong.

Fashionable revisionist history says the Fed didn’t need to take rates to 19% to crush inflation. Yet for a decade, every time inflation abated and the Fed eased policy, prices rose even higher.4

And who can forget the Whip Inflation Now campaign? Am I right?

Government-buttons, bowling ball bags, and even WIN branded footballs pushed Americans to fight 1974’s “Public Enemy #1,” rising prices. McDonald’s ran a Happy Meal ad showing how good fighting inflation tasted. A young Alan Greenspan remembered thinking, “This is unbelievably stupid.”

Mad Max became the most profitable film of all time in 1980 (a record it held for nearly 20 years) by portraying the end of the world as we know it. Having read nearly every piece of financial advice published in the 1970s-80s, I can tell you everyday Americans gave up believing prices would normalize. Financial strategies got ever weirder. “Get rich in real estate” gurus exploded onto the scene with a race to see who could buy houses for as close to $0 down as possible. The social contract was under immense strain. The impossible was coming into focus.

When one sees inflation, one cannot unsee it: the social chaos, the political crises, the fat tail risk that whips society into frenzies. The reigns of power get offered to failed painters and school teachers.

Wallich understood that confident Keynesians were playing with inflationary fire, like children who didn’t understand they might burn down the barn.

Behavioral Economists argue that people are crazy because we put lived experience above data.

But lived experience is data, the previous results from an experiment applying a strategy against uncertainty in real time. N = 1, sure, but not 0.

There are times when the most rational thing to do is not to optimize for the likely, but to protect against the overwhelming scale of the unlikely. Those who’ve seen the bad event know this, and behave accordingly.

Humans, not wrongly, sometimes understand that it is the impact of the event, not its likelihood, that matters. If the aliens come, insurance does you no good. If the layoffs do, an overabundance of cash may be sub-optimal, but is it crazy?

To quote Nassim Taleb,

“The market is like a large movie theater with a small door. And the best way to detect a sucker is to see if his focus is on the size of the theater rather than that of the door.”

Blindspot #1: dismissing the scale of the improbable.

Behavioral Finance and History’s Longest Bull Market

Blindspot #2: Behavioral Economics has no working theory of time.5 Or, if they do, it seems to be that things always work when given enough of it.

The old religion professed faith in a sane, Intelligent Investor who could beat Mr. Market, a manic depressive of high-highs and low-lows. The lascivious Ben Graham wrote these scriptures. Warren Buffett spread the good news.

But the new gods destroyed faith in savvy individuals, replaced by trust in a long-term rational market that rewarded patience and balance. Nearly all behavioral financial advice boils down to avoiding impulsive behavior and investing for the long term.

Why?

Because, from 1982 until early this morning, we lived through the longest bull market in human history. For the entire lives of Behavioral Finance scholars, the stock market has gone up and to the right, and the few times it did not strategies like 60/40 stock/bond splits offset the dips. Pity those who hedged their bets too much while values soared. They got Left Behind with Nicholas Cage (side note: did you know he starred in that? I didn’t).

Yet faith in markets to perpetuate what they have done for only a relatively short period is the irrationality of a discipline rooted in studying the irrational.

Markets, in this telling, are logical distributions of chance that cluster around a bright future.

But the future of the market was, and is, unknowable. Saying that the clear lesson of history is to trust the long term “rational” market outcomes is, well, wrong. The returns from institutions depend on the quality of those institutions, and for much of history the promise of compound returns were Gnostic gospels at best.

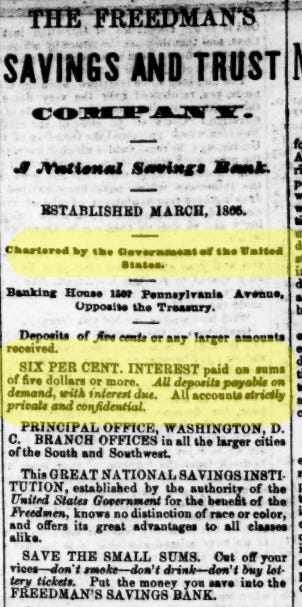

Ask the roughly 100,000 freed slaves who took the promised 6% returns from the Freedman’s Bank, chartered by Congress and advertised not-so-subtly as government guaranteed. It wasn’t. Few saw any yield at all, and the 60,000 who couldn’t get their money out in time waited nearly a decade to get 62 cents on the dollar back: 38% losses. From a savings account!

There have been plenty of stretches where long-term investing failed. As I pointed out in my book,

“Simply buying a house and saving 10 percent in stocks around 1870 would have left you wiped out four separate times. A recent study covering 125 years showed that Americans saving a whopping 20 percent of their annual incomes in stocks would have failed to survive retirement nearly half of the time. The only savings rate that never failed was over 40%.”

I am NOT a doomer. In fact, I’ve been mocked for my optimism.

But if you eye roll my N = 1 argument for blind spot #1, I will raise you this: N = 40 years isn’t a sample size in my line of work. As a historian, that’s a rounding error.

Behavioral Finance clusters a few generations of long-term bull market growth and substitutes it for a theory of financial time.

By the 2010s, even Kahneman thought this way. Most naive stock pickers, he showed, sold winners but held on to losers, hoping prices would come back (the disposition effect). You should do the opposite because of the “well documented market anomaly that stocks that recently gained in value are likely to go on gaining at least for a short while.”6

Winners keep winning, so keep them. Losers lose; ditch ‘em. This is statistically true, and one of the best documented investment strategies in finance.

Except when it isn’t.

From the CFA Institute:

The Achilles heel of momentum, however, remains its crash risk. Momentum strategies are vulnerable to sharp reversals, particularly during market regime shifts. We document maximum drawdowns as large as –88%

Losing 88 cents of your dollar? Yikes.

Those who live through recessions, behavioral economists find, are less likely to invest in stocks, which scholars treats as a failure of rationality, since obviously the future of the stock market is always bright… eventually.

By treating the long term future as knowable, or at least mostly assured, those who hedge against alternate endings get labeled “irrational.” But they are not, at least not always. They are aware that you can’t predict the future nearly as neatly as you can point to the past.

One of example in Behavioral Economics Guide 2026 shows that Baby Boomers overpaid roughly $22 billion by choosing fixed rate mortgages instead of adjustable rate ones (ARMs) because the future rates would be lower. But someone choosing the exact same strategy (an ARM) in 1972 was desperately wishing they had locked in their mortgage rate before they took off. The paper estimates that fixed rate families were better off to the tune of $7,700 in 1972, but the same strategy in 1981 backfired by a whopping $25,000. Those 1980s homebuyers should have gotten an ARM. The logical person would rather protect against a $25k loss than chase a $7k gain.

What the referenced paper does not do is study what would have happened if rates had kept going up, especially up by a lot.

“Silly goose! This is America! Stocks go up and prices come down! We would NEVER let inflation stay above 10%!!!!”

But there were people in the early 1980s explicitly saying 10% inflation was fine and expecting it to last in perpetuity. Fed Governor Teeters stopped voting for rate increases after 1979 because she felt the medicine for high inflation was worse than the disease. Personal finance gurus like Sylvia Porter told people to make their peace with high prices because it was the new normal.

So Americans bought expensive hedges against rates going up, because it was conceivable that they would. The mistake is only clear in hindsight. They faced time going forward.

The unknowable future doesn’t have to compound at 7% or revert to anyone’s mean.

Behavioral finance’s great insight was that individuals substitute their own subjective lives for logic in decision making. But it then turns around and treats the recent past as the entire data set for predicting future outcomes, which are inherently not bound to that past. A person may be irrational to worry about a 10 Sigma event from the mean, but it is equally irrational to assume everything must hover near it forever.

The past does not get to tell the future what to do.

In history, the mean doesn’t pull. It has no gravitational force.

So what?

Fair question. A few quick closing thoughts

Not all behavioral economists are this way: I don’t think I’ve made a strawman, but there certainly are excellent behavioral economists and practitioners who think far more holistically about life and decision making. Here is one, and a retirement-specific book out next year by McQuarrie and Bernstein is excellent (preorder here).

Don’t dismiss their fears: Probabilities don’t keep people up at night. Scale does. Acknowledge the rationality of the low probability, high impact worry. Maybe all those T-Bills help them manage the anxiety of a bad boss. And given the new government UAP files, perhaps we rethink Alien Abduction Policies. (I kid, I kid! They can’t payout while your agent is stuck inside the mothership!)

Sell downside protection, even when suboptimal: Yes, most hedges (lower performing assets, annuities, etc.) underperform bull markets. So?

Running with the bulls is exciting (in Pamplona or Wall Street), but have you ever tried running away from a bear?

Ponder that.

Buy the National Bestseller!

Order on: Amazon | Barnes & Noble | Bookshop.org | Books A Million

The Heavens Gate cult members who committed suicide had, oddly given their final choices, purchased insurance against alien abduction, impregnation, or murder. https://www.latimes.com/archives/la-xpm-1997-03-31-mn-43918-story.html

I’m using these terms interchangeably though there are subtle differences.

The paper referenced shows that previous inflation experience predicts Fed Governor rate votes, a brilliant insight. The dig at Wallich is subtle, and at first I thought I might be over-interpreting the point, but the book’s own QR code enabled AI Summary states that “despite having gotten the best economic training and having access to the best economic data and models,” as if hawkishness and “best” were opposites, Wallich dissented from rate cuts. The point seems clear: those without Wallich’s experience saw clearly, and Wallich could not. I would point out that relentless dissent need not be viewed negatively, and is a prerequisite for being prophetic. Alain Samson, ed., The Behavioral Economics Guide 2026 (2026)

I am agnostic on monetarism. How the ball ended up in the strike zone is less important to me than calling balls vs. strikes. Drechsler’s argument is genuinely intriguing, and of course the S&L Crisis was collateral damage. See William Greider, Secrets of the Temple: How the Federal Reserve Runs the Country (1989).

an objection to this might be that Behavioral Economists simply imports standard economic theories of discounting. But that is exactly my point. Discounting ties financial decision making in the present to time by holding that a dollar today is more valuable than a future dollar. Therefore, investment decisions about future dollars must convert future values into their present value via applying an expected discount rate. Behavior finances argues people are bad at it. I argue that in “expected discount rate,” expected is doing a lot more lifting than people think.

Daniel Kahneman, Thinking Fast and Slow (2011), 345.