I wish I was poorer ...

but a housing crisis is a terrible thing to waste

“Inflation is not all bad. It has allowed every American to live in a more expensive neighborhood without moving.” US Senator Alan Cranston.

Cranston was a character, perhaps the only American ever sued by Adolf Hitler in US court (successfully, nonetheless). Cranston knew German and the first American edition of Mein Kampf had, um, softened the message. Cranston sold half a million copies of his own, more accurate, translation until copyright law got in the way. Not the point, but worth remembering.

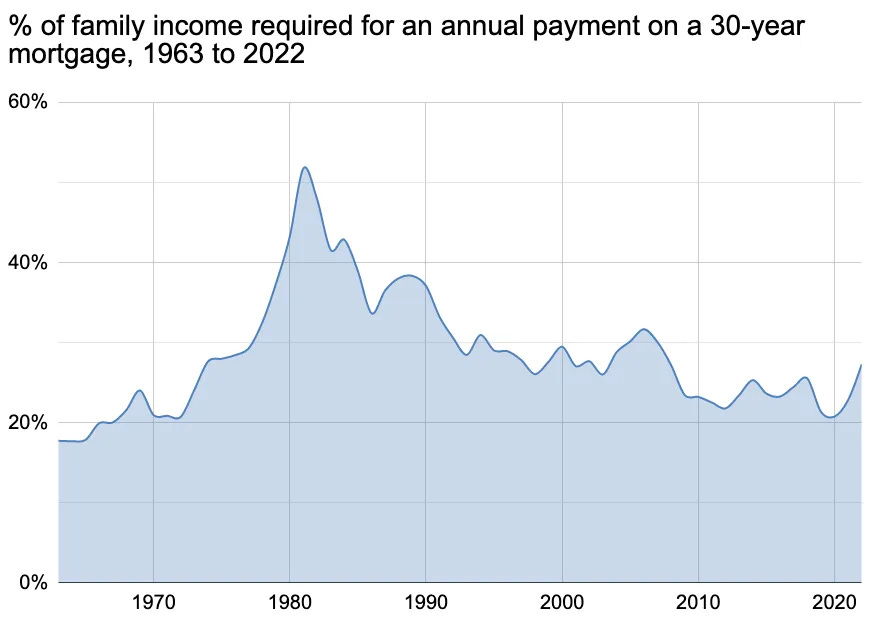

Cranston was also the son of a successful land developer and knew real estate well. He looked around and saw a problem not unlike today’s: neighborhoods became more exclusive without moving an inch. By 1981, with interest rates at 16%, a new mortgage cost 52% of median household income.

The graph below shows Nikita Sokolsky’s explanation of the math. In a follow up post, he found it was even worse for 1981 Seattle, where payments cost 67% of income. In Miami, it was 81%.

We have a housing crisis today. It is not the first, nor is it the worst. In the late 1940s the housing shortage was statically 2x today.

Thanks, Professor! I’ll sleep in my parents’ basement in joy and splendor knowing it used to be worse!

Fair.

To make history useful in 3 ways, let’s:

1) Explain why housing prices got messed up

2) Explain how to fix it

3) Since no one is going to solve it soon, explain how to thrive anyway

Idea #1: Home prices going up is historically weird

In 1990, homes in Pittsburgh, Atlanta, and Dallas cost the same (inflation adjusted) as they had in 1890. Homes in St. Louis didn’t exceed their nineteenth century values until 2003. For 100 years, house prices stayed the same.

The only places costs rose had local housing shortages: LA, NYC, DC and the easily abbreviate-able mega cities. People moved in faster than housing went up, so supply became more valuable. To be fair, half of the land around San-Fran is Pacific Ocean and Manhattan’s 1.6 billion tons of housing is sinking into the Atlantic one. But in most places, sink-proof land, lumber, and carpenters were plentiful so prices stayed the same.

Then 2008 happened, and everyone stopped building all at once. The whole nation turned into abbreviation-land. Existing homes got more expensive just by sitting there. Cheap money pushed everyone to bid up the left over houses, and now starter homes cost $1 million in over 200 cities. We turned a few regional housing shortages into a big, let’s hold hands and do this together, national one.

Experts debate how many homes we need. Two million? Five? Erdmann’s Housing Tracker says its 15 million units, which seems high until you realize that’s just a 10% shortage. However measured, its far more than we can quickly build. That’s a pickle.

Idea #2: Housing Avengers, Unite

Building code complexity, “Vote No!” button-clad residents at council meetings, and lawyers made it functionally illegal to build new things in desirable places. Construction Physics calls this “The Great Downzoning.”

What really went up was the price of good land you were allowed to build on, not the price of the houses. Homeowners are actually landowners, anti-heroes demanding a toll to cross the bridge from Renters-ville to Houselandia because they already paid theirs and need a refund.

The solution? Build an awkward alliance of developers who want to build, renters who want to buy, and homeowners burdened with skyrocketing tax bills who need to share the burden. Assembling this team portends a large political lift. It requires developers willing to build something aesthetically less awful, renters avoiding stupid placebos like rent control, and politicians who can spread the tax burden out wisely while resisting voter backlash.

Good luck with that.

In red areas, developer-funded Republicans clash with locals worn out by non-stop slash & burn tract homes. In blue ones, it’s Abundance Democrats pleading with wealthy HOAs to allow any growth at all. We can’t unite because the core components of Team YIMBY are separated by the Quantum Realm of Blue/Red states.

Idea #3: While Waiting for Ezra Klein …

You’re living inside a problem everyone wants solved but no one can, at least not soon. While our eyes scroll podcasts for deliverance, you have bills to pay.

How have Americans dealt with these problems before? Did they get ahead, or just give up? The answer is you, quite literally, you. They persevered or you wouldn’t be here.

Put another way: you’re going to have to solve this yourself just like they did.

Strategy 1: Move more.

You are neither the first nor fourth American generation to face a housing shortage. The answer then may be the answer now: get up and go. For most of time, between one-in-three to one-in-five Americans changed addresses every single year. Today, it is one in thirteen. Our nation of strivers is hoping to strive close to grandma, and I get that. But great-grandma probably moved multiple times, and so should you given that you live in the largest free market zone in the world. There is opportunity for you somewhere, and many of those places have homes half the cost of where you are. People who leave California save nearly $700/month and are nearly 50% more likely to own a house.

Strategy 2: You aren’t going to like it.

It involves another “one-in-three” stat.

That is the percentage of homeowners who rented out rooms in their house to pay off the mortgage at any given time before 1900. By World War II it was still over 20%. Realtors advertised family homes with extra rooms as “terrific for income” because they added at minimum 10% to the family bottom line. Nearly half of unskilled workers afforded their homes only because of their renters, often 3-4 at a time.

It was the primary American mortgage payoff strategy for 200 years.

I told you that you wouldn’t like it. But consider the logic. By definition, a housing shortage privileges those who monetize space. Yes, it requires work, but your great-grandmother used to have to feed and wash clothes for renters (meals/laundry came standard). You just make sure they keep the music down.

Strategy 3: You REALLY aren’t going to like it

Today, the Year of Our Lord 2026, it is cheaper in most large cities to rent than to buy, though still cheaper to buy than to rent in most counties (think ex-burbs and the Midwest).

There are lots of good reasons to rent: you can leave for opportunity, spend less, and your dog gets to pee anywhere she wants. Maybe rent your home and invest the difference.

But you should absolutely consider buying someone else’s. This housing shortage isn’t going away very soon. At best we’ll hit population equilibrium in the late 2030s, but more likely the tipping point is well into the 2040s-50s. That is most of your investing lifetime.

Consider this quote from The Washington Post:

“It’s getting harder for renters to become homeowners. “Prices have gone up relative to income … A 20 percent down payment is a lot more money now than it was 30 years ago.”

That was 10 years ago, in 2016.

Or this, from MarketWatch:

“With home prices remaining high and mortgage rates rising, more people are being priced out of the real-estate market and are instead looking to rent.”

… 2006.

Remember: house prices going up is historically weird, but we’ve been historically weird for about 40 years now. Since 1982, home prices in the US have roughly doubled in real terms for all the reasons above. We live in more expensive neighborhoods without having to move. It’s the land.

This insight combined with the post-2008 housing price collapse is how I’m able to sit on my butt and write. Part of the way to manage through a housing shortage is to take advantage of it.

I doubt home prices ever double again, but if you’re waiting on them to crash by half, think again. There just aren’t enough of them, and the good ones are on the best land. Even if the population were to decline, as happened in Japan, we’ll see more people move to large cities because that is where the amenities, hospitals, and restaurants will have workers. Real estate in Raleigh is probably a lot safer than in rural Oregon.

Listen, I’m a liberal academic humanities professor at heart. Please a) understand how we got here, and b) encourage your local pro-housing heroes to unite as one. But in the meantime, you should c) consider which side of the housing wealth equation you want to be on.

Most of my wealth is in real estate, and I’m totally happy to see it go down. Solving the housing crisis would add roughly a trillion dollars to GDP. I’d rather have a smaller slice of a much larger pie. Go Team Abundance! But if you don’t act on the world, you sit around hoping it will act on you. At which point…

Help us, Ezra Klein. You’re our only hope.

Buy the Book!

Order on: Amazon | Barnes & Noble | Bookshop.org | Books A Million